1. MODEL VALIDATION

RsRL’s Model Validation service offers the industry’s most comprehensive collection of models and methods formulating strong governance frameworks and model management in a complex regulatory environment. We help institutions to enhance their ability to price any conceivable instrument using the most advanced methodologies and calculations. RsRL emphasizes in enhancement of institution’s model validation process to keep up with regulatory change and model complexity along with managing the risk exposures brought on by insufficient models. Our methodologies provide flexibilities in wide range of calibration processes to generate current standard market consistent valuations.

Optimized Numerical Ability

RsRL’s core expertise are at providing solutions with strong mathematical & intense computation ability. Our quantitative analysis is designed with industry’s best speed & accuracy towards rapid calculations of complex instruments.

Main features

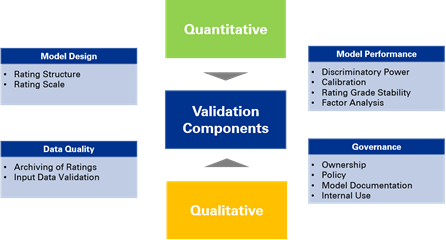

At RsRL, our expertise involves validating and testing Market risk valuation models and Benchmarking models to best market practice. Ensuring compliance of models with regulatory requirement and Back Testing of models. The validation of risk models and VAR cover the products and models as per the following table. These include model validation typologies and methodologies such as Discount Cash Flow Model , Market Price Model(computing greeks and risk for hedging purposes), Garmen Kohlhagen Model (pricing FX products), Markov Functional PDE Model etc.

2. MARKET DATA VALIDATION

To establish accurate models, it is essential to validate clean market data. RsRL brings years of experiences on validation of market data from primary level to complex data set.

Cutting-Edge Multi-Curve Framework Built in Python, Excel-VBA for Navigating the Shift to Alternative Reference Rates for (USD, EUR, CHF, JPY, GBP).

Helping to accelerate institution’s LIBOR transition to Alternative Reference Rates

| # | Curve Construction Practices in a multiple curve framework (all major International currencies) | Cross Currency Framework | Pricing of non-linear interest rate structures |

|---|---|---|---|

| 1 | A.OIS discounting curve construction in all G5 currencies (USD, EUR, CHF, JPY, GBP). | A.Cross currency curve construction. | A.Swaptions and Swaption Volatility surfaces. |

| 2 | B.Construction of projection curves for multiple tenures. | B.Cross currency swap pricing. | B.Caps and floors and their volatility surfaces |

| 3 | C.Construction of basis curves. | C.Proxy OIS curve construction for illiquid currency. |

3. XVA/PFE

RsRL provide industry’s most sophisticated analytical platform to manage counter party risk exposures in the form of integrating XVAs into deal prices. We use high standard hybrid model and robust Monte Carlo simulations towards comprehensive analysis of OTC derivatives and structured derivative products.

Main features

Case Study

Let us consider two financial products A and B have basic two components, i) cash flows, ii) option; and the product A could be denoted by X = (Xt)0≤t≤TX the cash flows and for B the cash flows could be Y = (Yt)0≤t≤TY . This research introduces four stages of modeling counterparty credit exposure with various cutting-edge frameworks and simulations and a sophisticated potential future exposure (PFE) quantification with a time-inhomogeneous parameterization of the forward LIBOR volatilities and analyzes its implications for the valuation of Bermudan swaptions as a callable valuation. In first stage the risk factor simulation depicts that one can place variable portfolio-specific simulation grid-points to reflect well specific events that are relevant for a portfolio such as coupon payments, exercise decisions and margin calls. Thus, one can use a portfolio specific simulation grid. In the 2nd stage we construct models for various instruments. We price the interest rate derivatives in the LIBOR Market Model (LMM), the LIBOR forward-rates, the instantaneous volatility of these rates and the instantaneous correlation between them are specified. The AMC PFE system uses regular Monte Carlo for risk factor scenario generation. In the instrument valuation step, it avoids Monte Carlo-within-Monte Carlo by estimating the continuation value of the product by regressing it on a set of observable financial variables at the valuation time. Most important part of this section is conditional valuation of the instrument such as European Swaption. Our model primarily approximates the actual term structure of volatilities with a curve from a given set defined by the parametric volatility specification and the structure of a continuous time Markov chain that modulates the volatility function. Then we emphasize the pricing counterparty through netting and credit valuation adjustments (CVA) in the final stage of the research project.

Finally, the motivation of our scenario generation techniques and the risks factors we portrait to the use of the Gaussian copula and of implied correlation had all been so far untouched by the quantitative community. We either work-on the new reasons of Gaussian copula model extensions such as random recovery.

4. VaR

RsRL provide extensive solutions to help institutions through the review process required to gain regulatory approval for using an internal Value-at-Risk (VaR) model as well as Stressed Value-at-Risk (SVaR) model to calculate regulatory capital.

RsRL’s question to BIS and other regulatory bodies is: Are present risk measures and capital requirements adequate? The truth here is that we still do not know. They may be, but we will only know about inadequacy if they are breached. Short of 100% reserves this is the best we can do. The scary thing is the concept of adequate capital requirements. If people think such a thing exists then they are simply deluding themselves. Adequacy here is a relative concept. Even 100% reserves. depends from leverage. Leverage 15/20 times and even 100% does not make you safe. The risk measure that is in use in the financial industry is Value-at-Risk or VaR. Mathematically speaking this is a quantile at accepted failure level (say 0.1% or 0.5%). The required capital is then calculated in order to have a failure probability lower than the VaR-level. No concern of what happens below that level. This is the same as given a free option to the company. To put it in an extreme way: in case one goes bankrupt, make sure it is a very big bankruptcy. The lower you might get, the higher one can come with the expected benefit. Positive parts and negative parts are in equilibrium. Some have created VaR- like measures which integrate the Tail (or the square of the Tail, etc.) to distinguish the cases as you note. This does give more information, and even can buy one out of the failure at subadditivity. There is a limit, however, to the information content of a single point (or two or three points) on the real line. A complete function (like a distribution function) provides infinitely (literally) more information.

RsRL VaR Methodology

Step 1: We need to check what the existing process that is being used for computing VaR. Is it risk based, grid based or full-revaluation?

Step 2: Identify all key risk factors of all products under our scope of work. Check whether the relevant model generates risks with respect to these key factors or not. If we dont have risk computation for some of the risk factors, do we consider these risk factors under a RNIV (Risk Not in VaR ) framework?

Step 3: Check whether the risk feeds from the pricing system to the risk system are correct.

Step 4: Check whether the PnL calculation for all these risk factors are correct. As an example, when a big US investment bank made an error in the PnL calculation by a factor of 2. This resulted in the bank having to pay a substantial fine for this error.

Step 5: Check that the implementation of the VaR formula is correct.

Step 6: Identify all assumptions made for risk factors. For example, has the term structure for certain risk factors been considered or not?

Step 7: Give an assessment as to how much all the assumptions have impacted the VaR numbers.

Step 8: If there is a significant impact on the VaR numbers due to certain model assumptions, we may have to utilise an Overlay.

Step 9: If a risk based approach is used for VaR computation, a comparison with full revaluation would give an assessment as to how effective is this risk based approach.

Step 10: The main outputs are the approval of the VaR model, the list of all the key model assumptions and the restrictions/compensating controls (an Overlay) around the utilisation of the VaR model.

5. FRTB

The global financial crisis exposed the shortcomings of market risk management practices of the trading book. In January 2016, the Basel Committee for Banking Supervision (BCBS) overhauled the approach to assess capital requirements with the Fundamental Review of the Trading Book (FRTB). With a 2022 deadline, FRTB is expected to have significant impact on financial institutions and financial markets in terms of infrastructure, capital requirements and operational controls. Banks must adhere to the rules of the fundamental review of the trading book to avoid higher capital requirements. The FRTB defines two separate approaches for quantifying capital requirements for market risk Internal Model Approach (IMA) and Standardized Approach (SA). FRTB affects many areas including front office, product control, data and technology. FRTB is a major change to the banking industry current market risk management practices, including a stricter boundary between the trading and banking book to a more stringent approval process for the use of an internal model.

RSRL FRTB

RsRL FRTB is designed with complex set of regulations to bring enhancement in decision making for front and middle office duties of market risk processes and technology. The goal of RsRL FRTB is to perform impact assessments and regulatory scenario analysis to help Banks in achieving well informed strategic decisions. In order to attain maximum capital efficacy, RsRL FRTB provides flexibility to determine optimal trading desk configurations and model choices whether it is IMA or SA. One of the competitive advantages for Bank is to gain positive P&L impacts by implementing and accelerating FRTB readiness and RsRL is at forefront to comply FRTB for them in the Gulf region. Due to perceived complexity of implementing internal model approach, RsRL FRTB emphasizes more on standardized approach. At the same time, switching from SA to IMA, could lower capital requirements substantially.